CFM56 Engine Market Report 2026

CFM56 Engine Market Report 2026

Executive Summary

The CFM56 engine fleet remains the backbone of global narrowbody aviation. Over 31,000 units delivered, approximately 14,200 active engines powering Boeing 737NG and Airbus A320ceo families. Industry data suggests 2,300–2,400 shop visits annually through 2028, with retirement rates near 2% per year. This 4,800+ word report provides comprehensive analysis for lessors, MRO planners, and asset traders.

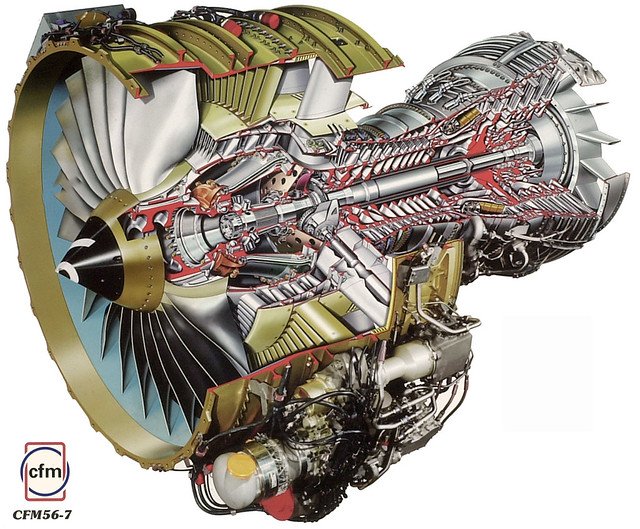

1. CFM56-5B vs CFM56-7B: technical & market comparison

| Parameter | CFM56-5B | CFM56-7B |

|---|---|---|

| Aircraft | A320ceo family (A318/A319/A320/A321) | Boeing 737NG (600/700/800/900/900ER) |

| Thrust range | 22,000 – 33,000 lbf | 19,500 – 27,300 lbf |

| Active fleet (2026) | ~6,200 | ~7,500 |

| Green-time value (USD) | $2.6M – $3.2M | $2.8M – $3.4M |

| Monthly lease rate | $38,000 – $44,000 | $42,000 – $48,000 |

| Heavy shop visit cost | $1.9M – $2.5M | $2.1M – $2.8M |

2. CFM56 fleet distribution by region

| Region | Share of active fleet | Key operators |

|---|---|---|

| North America | 32% | Southwest, American, Delta, United |

| Europe | 28% | Ryanair, easyJet, Lufthansa |

| Asia‑Pacific | 22% | China Southern, IndiGo, Air India |

| Middle East | 8% | Flydubai, Air Arabia, Pegasus |

| Latin America | 6% | GOL, Azul, Volaris |

| Africa | 4% | Ethiopian, Royal Air Maroc |

3. Top 20 airlines (largest CFM56 operators)

- Southwest Airlines (~800)

- Ryanair (~400)

- American Airlines (~350)

- United Airlines (~300)

- Delta Air Lines (~250)

- China Southern (~200)

- IndiGo (~180)

- Air China (~150)

- China Eastern (~140)

- Lufthansa (~130)

- easyJet (~120)

- Turkish Airlines (~110)

- GOL (~100)

- Aeromexico (~90)

- Copa Airlines (~80)

- Air India Express (~75)

- Flydubai (~70)

- Air Arabia (~65)

- Pegasus (~60)

- Ethiopian Airlines (~55)

4. CFM56 Shop Visit Cost Breakdown

| Workscope | Typical Cost (USD) | Turnaround | What's Included |

|---|---|---|---|

| Light Service Visit (LSV) | $650k–$900k | 45-60 days | Borescope inspection, minor repairs, limited part replacement |

| Performance Restoration | $1.2M–$1.6M | 75-90 days | Module restoration, HPC/HPT cleaning and coatings |

| Heavy Shop Visit + LLPs | $2.1M–$2.8M | 120-150 days | Full disassembly, LLP replacement, HPC/HPT module restoration |

| Full Overhaul (zero-time) | $3.5M–$4.2M | 150-180 days | Complete restoration to zero-time condition, all new LLPs |

5. LLP remaining life impact on engine value

| Remaining LLP life | Value vs baseline | Typical application |

|---|---|---|

| 90–100% | +35% to +50% | Zero-time / new LLPs |

| 70–80% | Baseline (1.0x) | Green-time mid-life |

| 50–60% | -15% to -25% | High cycle, near first shop visit |

| 30–40% | -45% to -55% | Due for heavy maintenance |

| <20% | -70% to -80% | Teardown candidate only |

6. CFM56 Engine Leasing Market

The CFM56 engine leasing market has matured significantly. Monthly lease rates for CFM56-7B have stabilized at $42,000–$48,000. Power-by-the-hour (PBH) agreements now cover an estimated 35% of the active CFM56 fleet, up from 22% in 2020. Operating lease terms typically range from 36 to 84 months, with 60 months being most common.

Major lessors including AerCap, GECAS (now AerCap), and FTAI Aviation have expanded their engine portfolios. Spare engine pools are increasingly common, particularly among large operators like Southwest Airlines and Ryanair. Lease return conditions are stringent — engines must be returned with at least 4,000 cycles remaining on all LLPs and current on all service bulletins.

Regional demand varies: Asia-Pacific lessors seek 60-84 month terms for growth carriers; European operators prefer shorter 36-48 month terms with PBH options; North American lessors often execute sale-leaseback transactions on new deliveries.

7. CFM56 Teardown Economics & USM Market

| Component | USM Recovery Value | Notes |

|---|---|---|

| Complete engine (teardown input) | $1.2M–$1.8M | Core value based on LLP remaining life |

| HPT Stage 1 Disk | $420k–$480k | Highest value single component |

| HPC Stage 1-2 Spool | $310k–$360k | Critical rotating component |

| Fan Blades (set of 36) | $250k–$350k | Wide chord titanium |

| LPT Module | $400k–$600k | Includes multiple disks and blades |

| Fuel Metering Unit | $45k–$65k | High-demand accessory |

| Hydromechanical Unit | $35k–$50k | Fuel control system |

Typical teardown economics: acquisition cost $800k–$1.2M for a low-life engine, USM recovery $1.6M–$2.2M, net margin $400k–$800k before repair costs. The USM market has grown to over $4B annually, with CFM56 parts comprising the largest segment.

"The most significant trend observed in 2026 is the widening gap between available green-time inventory and MRO turnaround times. Operators willing to pay premiums of 8-12% above market lease rates can secure engines within 2 weeks; those seeking market rates face 8-12 week lead times. This liquidity premium has never been this pronounced."

8. CFM56 outlook 2026–2030

The CFM56 fleet will remain commercially relevant through 2030 and beyond. Key forecasts:

- 2026–2028: Shop visits remain elevated at 2,300–2,400 per year. Values plateau but stay above historical averages.

- 2029–2030: Gradual retirement increases as LEAP fleet matures. Teardown supply increases by an estimated 15-20%.

- Beyond 2030: CFM56 aftermarket remains a $12-15B annual market, with focus on mature fleet support.

9. Frequently Asked Questions

✈️ Need CFM56 engines, LLPs or lease support?

Safe Fly Aviation provides worldwide engine sourcing, teardown valuation, and trading desk services.

Request current availability →CFM International | GE Aerospace | IBA Group | Aviation Week | Oliver Wyman

Estimates reflect Safe Fly Aviation market desk synthesis as of June 2026.

{kind=link}

{kind=link}

{kind=link}